Government has to open purse-strings to get new highways off the road

December 24, 2015

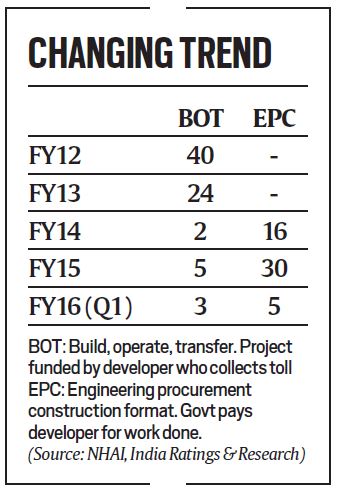

7,500 km at completion risk, trend shifts to govt-funded format.

The road sector is being widely touted as the only glimmer of hope in a bleak core sector narrative, but the numbers tell a different story

On December 2, creditors of Hyderabad-based road developer IVRCL Ltd decided to convert their loans to the company worth Rs 7,500 crore into a majority equity holding. The lenders, led by State Bank of India and IDBI Bank Ltd, invoked the strategic debt restructuring (SDR) provision that allows banks to take over the management of a firm after converting debt into equity in cases where debt restructuring has failed or is near failure.

In August, Gammon Infrastructure Projects Ltd agreed to sell six roads among nine infrastructure projects to BIF India Holdings Pte Ltd for Rs 563 crore, taking advantage of a newly introduced regulation to ease the exit of developers of operational road projects. On November 23, Gammon India Ltd’s lenders decided to invoke the SDR norms and convert a part of its Rs 15,000-crore debt into majority equity.

The road sector is being widely touted as the only glimmer of hope in a bleak core sector narrative, but the numbers tell a different story. An estimated 7,500 km of highway projects have been deemed to be at high risk of not being completed, including 5,100 km under construction and 2,400 km of operational sections that were awarded mostly between fiscals 2010 and 2012 on the Build, Operate, Transfer (BOT) format.

Estimates prepared by the research arm of rating agency Crisil show that of the projects under construction that are at high risk, around 50 per cent are due to significant cost over-runs and weak wherewithal of sponsors.

Finding it difficulty to award Highway sections to private developers, the roads ministry has resorted to a sharp shift from the BOT model to the government-funded Engineering Procurement Construction (EPC) format. The EPC model is less capital-intensive and the developer is largely insulated from the traffic risk — the government makes the payment and the developer’s responsibility ends with delivering the completed project.

Under the BOT model, where the developer funds the project and earns returns from toll collection for the duration of the concession, the capital is locked in for a long period with the risk of revenue not adequately covering for construction and debt servicing costs. Road Transport and Highways Secretary Vijay Chhibber told The Indian Express that about 80 per cent of road projects are being offered under the EPC route currently, with BOT and hybrid annuity accounting for the rest. “As the market changes, we will increasingly move away from EPC and in favour of hybrid annuity and BOT,” he said.

The hybrid annuity model is a mix of the EPC and BOT models, where the road authority will provide an initial grant of up to 40 per cent of the cost with the developer chipping in with the rest and completing the project. Data from India Ratings and Research — a unit of Fitch Ratings — shows that 21 highway projects worth Rs 26,000 crore failed to attract bids over the last two fiscal years.

As a result, the National Highways Authority of India (NHAI) had to fall back on EPC contracts to plug the gap — from nearly an all-BOT road model during 2008-09 and 2012-13, the share of BOT dipped below 15 per cent in 2013-14 and 2014-15. For instance, out of 7,980 km length of national highways awarded during the last year, just 700 km had gone on public private partnership mode and the rest were all EPC projects. But even if a large-scale shift to EPC were to happen, there are bound to be tremendous constraints on funding. A parliamentary panel review report in December flagged that NHAI was able to spend only Rs 6,208 crore out of Rs 23,691.8 crore, or about 26 per cent, allocated during 2014-15 at the Revised Estimate stage (in the budget for 2015-16).

The official contention of the roads ministry, though, is that during 2014-15, the NHAI recorded total cash outflow or expenditure amounting to Rs 23,696.19 crore and that the company actually used borrowings amounting to Rs 2,876.40 crore to bridge the gap between resources from the government and its cash outflows.

While there seems to be some pickup in project awards, the outlook for under-construction projects is turning more bleak. “Under-construction projects require equity and cost-overrun support of around Rs 28,500 crore over the next two years. Of this, about Rs 16,000 crore could be stumped up from internal accrual of sponsors and sale of stake at the special purpose vehicle level. That leaves a significant shortfall of Rs 12,500 crore,” said Sudip Sural, senior director, Crisil Ratings, who worked on the roads sector report.

On the issue of projects awarded between 2010 and 2012 being at a high risk of not being completed, Chhibber admitted that the government has worked hard to work a way around the legacy issues that were dogging progress of road projects. “The real gamechanger is the recognition within the government that we may have also contributed to the languishing projects, in terms of delays in clearances and land acquisition. So, we’ve taken a decision that to the extent that the delay is on account of such factors, we will compensate the developer. This is a major policy shift… the acceptance of the fact that the government has not met its side of the bargain,” he said. He also said that in some cases, the concessionaire may have taken out more money out of the project and is now not interested in its completion.

In such cases, Chhibber said the ministry will not stop short of taking action against developers, “even to the extent of cancellation of contracts”. Atul Punj, chairman, Punj Lloyd Ltd, a construction services player in the infrastructure sector, told The Indian Express that while there was an uptick in the highways and the power transmission sectors, most other infrastructure segments were still struggling. According to him, the clubbing of the construction sector within the overall infrastructure bracket for funding purposes was undermining the recovery. This is more so, he said, because banks were at the upper end of their limits on lending to the infrastructure sector, leaving the construction sector, which shoulders the primary load of setting projects into motion, badly hamstrung.

Pending disputes: Rs 25,000 crore Disputes are another issue that are hampering the completion of road projects. Data from the road ministry shows that 112 cases involving Rs 25,000 crore were pending under arbitration between the NHAI and developers till end-April 2015. The disputes are typically accompanied by lengthy arbitration, something that private players feel drains them badly. Added to this is the fact that an underdeveloped bond market has forced PPP road projects to mainly depend on debt from commercial banks, something highlighted by the Reserve Bank of India Governor Raghuram Rajan, who cautioned banks of their high exposure to the sector and underscored the need to deleverage.

By February 2015, the total deployment of gross bank credit in the road sector was Rs 1.67 lakh crore, 384 per cent up from FY08. The infrastructure sector was identified by RBI, in 2013, as one of the five sectors with a high level of stressed advances. Wooing investors Apart from the hybrid annuity model, introduced for projects granted from October 1, 2015, the government has been looking at other ways to boost investor appetite.

In August 2015, the Cabinet Committee on Economic Affairs cleared a proposal to allow infrastructure companies — essentially in the road sector — to divest 100 per cent of their equity after two years of completion of construction for all projects given as per the BOT model, irrespective of the year the contract was handed out. This was to allow companies to use the funds from the sale of equity to invest in other projects as well as repay their debts. But road developers say it’s tough to hold on to the asset for even two years after completion of construction, as the debt goes up because of cost escalations due to inordinate delays for land and other clearances, legal disputes and arbitration proceedings. The solutions, according to a Maharashtra-based private developer, are far from optimal.

Sources: Indian Express

Government to rate national highways on 20 parameters

November 23, 2015

NHAI chairman Raghav Chandra has said that the project will cover the entire NH network and one of the key parameter will be the green cover and beautification along the NHs.

NEW DELHI: Considering that most stretches of highways in India don’t provide much comfort to commuters on different parameters such as smoothness of the ride or sensibly designed entry/exits, the government will now start rating all national highways (NHs).

The road transport and highways ministry is preparing about 20 parameters for objective assessment of NHs from time to time. They include, commuters’ comfort, safety, aesthetics and other facilities for pedestrians. These will work as guidelines for both the commuters and the government, sources said.

NHAI chairman Raghav Chandra has said that the project will cover the entire NH network and one of the key parameter will be the green cover and beautification along the NHs.

This massive exercise is being undertaken for objective assessment of highways to identify the worst stretches that need immediate attention of government. “It will be an objective way of measuring things and will help avoid a situation where government undertakes works for political reasons. We are identifying the criteria, which will largely cover the width and quality of road, what is the satisfaction level of all types of road users and safety features as well,” said a road transport ministry official.

The proposal gains importance considering the fact that Prime Minister Narendra Modi has emphasized the need to develop highways and all other related facilities to ensure that people “enjoy” the drive on any stretch of NH.

Sources said though across the world no country has rated its NHs or express motorways, India has planned this since many highway stretches here are of one and two lanes. “Either we take a decision that no NH will be less than four lanes or we have to put some mechanism in place for objective assessment of the existing stretches. Rating of highways will also create greater public awareness,” said an NHAI official.

Source: The Times Of India

Electronic toll collection on highways: NHAI signs pact

September 20, 2014

NHAI-promoted Indian Highways Management Company Limited (IHMCL) has inked a pact with Axis BankBSE 0.57 % for services related electronic toll collection, which the government plans to introduce pan-India.

Considering the complexities and geographical spread, the nationwide electronic toll collection (ETC) would be first of its kind in the whole world.

“IHMCL, a NHAI promoted company and Axis Bank has signed an agreement for provision of Central Clearing House (CCH) services and sale of FASTag, for Electronic Toll Collection (ETC) at the Toll Plazas on the National Highways,” an official statement said today.

It said ETC system on Delhi – Mumbai stretch of the national highways will be made operational by the end of this month and a nationwide rollout will be carried out by the end of year.

Earlier this year, IHMCL had signed agreement with ICICI Bank also and it has two banks now to perform clearing and settlement of electronic toll transaction, which is a key requirement for electronic toll collection.

This is subsequent to the initiative taken by the Ministry of Road Transport & Highways, NHAI and IHMCL for implementation of unified Electronic Toll Collection on Indian national highways.

Electronic Toll Collection enables road users to pay highway tolls electronically without stopping at the toll plazas.

“The unique number of the RFID FASTag affixed on the wind shield of the vehicle will be read by the readers fitted in the dedicated ‘ETC’ lanes of plazas and the toll will be deducted automatically,” the statement said adding this will help in reducing congestion at the toll plazas and enable seamless movement of vehicles on the national highways.

The Ministry has decided to roll out ETC programme in the country under the brand name “FASTag”.

The dedicated ETC lanes will have colour coding for distinct identity recognised as “FASTag lanes”.

ICICI Bank and Axis bank, engaged for providing CCH services, would distribute RFID based “FASTag” through their franchises/agents and at points of sales near the toll plazas

Road users can enrol and get “FASTag” affixed on their vehicles at designated toll plaza locations or Point of Sale (POS) stations of Axis bank and ICICI bank.

Such type of highway tag brands are common in developed countries and are known by different names like “Eazee Pass”, “SunPass” in the US, “e-Pass” in Australia, “Salik” in Dubai etc

Anti-toll activists to hold public debate with NHAI

September 12, 2014

The National Highway Toll Collection Opposition Federation will convene a public debate with National Highways Authority of India (NHAI) officials on September 13 at Hanumanahalli toll point on the outskirts of Mulbagal.

Holding ‘irresponsibility and negligence’ of the NHAI and contractors responsible for accidents, the federation has exhorted NHAI officials to participate in the meeting.

It has also issued notices to the Chief General Manager (Technical) and project director of NHAI regional office, Bangalore.

Veteran freedom fighter and president of the federation H.S. Doreswamy will take part in the debate.

In a notice, a copy of which is available with The Hindu , the federation took exception to collecting toll fees without completing works as per the agreement.

The Deputy Commissioner on Tuesday said that a criminal case would be filed against NHAI authorities and contractors for negligence.

Source:The Hindu

Two revenue models proposed for bypass from Kazhakuttam to Karode

July 29, 2014

Thiruvananthapuram:

Annuity mode or tolling has been mooted to attract bidders to develop the 43.62-km stretch of the National Highway 66 (NH 66) bypass from Kazhakuttam to Karode into a four-lane carriageway.

Annuity mode or tolling has been mooted to attract bidders to develop the 43.62-km stretch of the National Highway 66 (NH 66) bypass from Kazhakuttam to Karode into a four-lane carriageway.

The suggestions had been made as at least five companies had shown ‘lack of interest’ to the request for proposal (RFP) floated by the National Highways Authority of India (NHAI) to develop the 26-km stretch from Kazhakuttam to Mukkola initially.

Opposition to toll collection in the State, its non-feasibility, and delay in handing over land for the 17.62-km stretch of the road up to Karode on the Kerala-Tamil Nadu border had been cited as the main reasons for the withdrawal of the companies.

An official of a company who participated in the RFP told The Hindu that the provisions to provide a link from the NH 66 to the proposed Kazhakuttam-Karode bypass had also affected the take off of the project, dragging on for over four decades now.

‘Financial closure’ was perceived difficult as toll volume would be low. Not many multi-axle vehicles moved through the stretch, qualified bidders had informed the NHAI.

Mostly, small cars would take the road and only 30 to 40 per cent of the road capacity would be used once it became a four-lane carriageway, he said.

The Public-Private Partnership Appraisal Committee had given the nod to take up the first 26 km on a public-private partnership (PPP) mode, for Rs.577.95 crore. The total project cost would be Rs.1,170 crore.

The bidders had also sought a revision of the design in view of the 16 road crossings proposed. At Venpalavattom, Chakka, Enchakkal, and Thiruvallom, vehicular underpasses had been mooted.

They had also told the NHAI that banks would give ‘financial closure’ to annuity mode as banks strictly followed RBI lending guidelines.

Land had been acquired for a four-lane stretch and to the extent of 45 metres on the Kazhakuttam-Chakka-Eenchakkal-Kovalam stretch. Fixing the fair value for the land in the Chenkal and Karode Blocks had been the major hurdle in completing land acquisition, sources said.

Source:The Hindu

No NHAI funds if Kerala develops NH stretches at 30 m: Gadkari

July 15, 2014

PTI, NEW DELHI

The Centre will not extend any assistance under the national highways programme if the Kerala government decides to develop NH stretches in the state at 30-metre width instead of 45 metres.

This was informed by Union Minister for Road Transport and Highways Nitin Gadkari to BJP’s Kerala unit president V Muraleedharan who met him at his office here.

“We are opposing the state government’s move. We informed the minister (Gadkari) that national highway should be 45 m and Kerala government should not be allowed to convert it into a 30-m national highway. He told us that NHAI funds would not be available for NHs less than 45 m wide,” Muraleedharan told PTI.

The Kerala government is keen on fast-tracking four-laning of 30-m highways to avoid the massive land acquisition that was needed if the width was 45 m or 60 m as in the case of other NHDP projects in the country.

Bowing to pressure from the state, the previous UPA government had agreed in principle to reduce the width of 829 km of national highways being developed from 45 m to 30 m.

Muraleedharan claimed that the state government wanted to tweak the rules on the pretext that it could not acquire land.

“It was a sort of a conspiracy on their (state government’s) part,” Muraleedharan said and alleged that “if it is allowed to have a 30-m road and the central government’s assistance is available, it will benefit many people who are in this contract.”

Big-ticket infrastructure projects in sight, all roads lead to PPPs

July 11, 2014

ENS Economic Bureau

The road sector got a major boost on Thursday as the government announced it would invest Rs 37,880 crore for the National Highways Authority of India (NHAI) and set a target of constructing 8,500 km of highways in the current financial year.

In his budget speech, Finance Minister Arun Jaitley said steps would be taken to encourage the private sector to partner with the government in executing big-ticket infrastructure projects. As a key step, he said, an institution called 3P India would be set up with a corpus of Rs 500 crore to help execute public private partnership (PPP) projects. For project preparation, NHAI would set aside Rs 500 crore, he said.

Setting an ambitious target of constructing 8,500 km of highways this fiscal, Jaitley said of the Rs 37,880 crore to be invested for highways, Rs 3,000 crore would be spent in the Northeast alone. He announced initiation of work on select expressways in parallel to the development of industrial corridors.

Jaitley said India has emerged as the largest PPP market in the world with over 900 projects in various stages of development. PPPs have delivered some iconic infrastructure like airports, ports and highways, which are seen as models for development globally. But considering the weaknesses of the PPP framework and rigidities in contractual arrangements, there is a need to develop more nuanced and sophisticated models of contracting and develop quick dispute redressal mechanism.

Stating that the Pradhan Mantri Gram Sadak Yojana, which began under the tenure of NDA-1, “had a massive impact” in improving access for the rural population, Jaitley said, “It is time to reaffirm our commitment to a better and more energetic PMGSY under the dynamic leadership of Prime Minister Narendra Modi. I propose to provide a sum of Rs 14,389 crore.”

After a dismal show in 2012-13, the Union Road Transport Ministry had scaled down its projects award target by nearly half to 5,000 km 2013-14. It could award less than 2,000 km projects in 2013-14. In 2012-13, the ministry was barely able to award 15 per cent of the targeted 9,500 km of highways on account of a number of factors, including delay in clearances and equity crunch by developers.

“The road sector constitutes a very important artery of communication in the country. The sector had taken shape from 1998-2004 under NDA-I. The sector again needs huge amount of investment along with debottlenecking from maze of clearances,” Jaitley said.

Arguing that metro projects have helped in de-congesting cities, he said Rs 100 crore has been earmarked in the budget for metro projects in Lucknow and Ahmedabad.

A National Industrial Corridor Authority, to be headquartered in Pune, would be set up with a corpus of Rs 100 crore to coordinate the development of the industrial corridors, with smart cities linked to transport connectivity, he said.

Saying development of ports is critical to trade, he said 16 new port projects are proposed this year. He announced allocation of Rs 11,635 crore for development of outer harbour project in Tuticorin for phase I.

Jaitley announced a new scheme to develop airports through PPP and hiked allocation for the Civil Aviation sector by over 11.4 per cent to Rs 9,474 crore.

Source-http://indianexpress.com/

Roads of trouble

April 7, 2014

RAHUL PRITHIANI

Road developers are in a tizzy as both debt-servicing ability and returns of national highway projects have come under severe strain as the economics has gone haywire because of low traffic, execution delays and cost overruns.

Over the past couple of years, traffic growth on national highways has slid precipitously, in conjunction with the economy and industrial production. An analysis of traffic growth across 15 national highway projects that have been operational for over three years revealed that overall traffic growth, estimated at 7-8 per cent between fiscals 2008 and 2011, slumped to 3-4 per cent in 2012 and to 2-3 per cent in 2013. In fiscal 2014 too, the traffic growth has been weak due to sluggish economic activity.

The culprit was commercial vehicle traffic, whose slowdown overshadowed a healthy 15 per cent average growth in passenger vehicle traffic during this period.

Special purpose vehicles

This deteriorating trend is also mirrored in the revenues of a dozen special purpose vehicles (SPVs) operating under the build-operate-transfer (BOT) model. Revenues of these SPVs have grown by about 12 per cent in the past couple of years. During this period, toll rates rose by 8-9 per cent per annul as these are linked to the wholesale price . But poor traffic growth negated most of the benefits.

The scenario is unlikely to improve much in the near-term. Road traffic has high correlation with industrial growth . While we expect IIP to recover in fiscal 2015 to about 4 per cent from the decadal low of about 1 per cent it hit in fiscal 2014, it will remain well below the long-term average.

Consequently, commercial vehicle traffic growth will be lacklustere and overall traffic growth on national highways will languish at 3-5 per cent in fiscal 2015. As almost the entire operating costs in a road project are fixed in nature, any variation in the traffic, especially during initial years, has a significant bearing on the project returns.

Slow traffic growth on national highways is not the only problem plaguing developers. Base traffic (in the first year of a highway’s operation) has been much lower compared to the NHAI draft project report estimates. To be sure, developers would have done their own math on traffic, including expected leakages and exempt vehicles, before bidding, yet they will be concerned about how wide off the mark the original estimates were.

Compounding these problems for road developers are delays and the resultant cost overruns. Of the 78 BOT projects completed between fiscals 2000 and 2013, more than three-fourths or 61 projects faced delays, with the average time overrun at 10.5 months. The situation has only worsened in the last couple of years. Execution hasn’t begun for about 33 projects awarded in fiscal 2012 .

The double whammy of lesser-than-expected traffic and cost overruns has severely impaired the debt-repayment ability of developers. For five of these projects, the average debt-service coverage ratio during the first five years of operations is estimated to be less than one. This means equity infusion is essential to ensure timely servicing of debt, especially since tying up for additional debt will be difficult in the current scenario. Returns for these road projects are also expected to be 8-14 per cent, much lower than the 22-26 per cent returns based on NHAI traffic and cost estimates.

The above-mentioned scenario is representative of most road developers. Clearly, road developers are being buffeted by problems from all sides and have very limited room for manoeuvre. Recently, the government offered some respite by relaxing exit norms and allowing for premium deferment in the case of stressed projects. However, it might turn out to be a case of too little, too late.

The author is Director, Crisil Research, a division of Crisil

Source- http://www.thehindu.com/

NHAI approves compensation package for land acquisition

March 13, 2014

SPECIAL CORRESPONDENT

Development of NH bypass from Kazhakuttom to Karode

The National Highways Authority of India (NHAI) has granted approval for a compensation package for acquiring land from Kottukal village for the development of the 43.62-km NH-66 bypass from Kazhakuttom to Karode on the Kerala-Tamil Nadu border.

The NHAI decision comes at a time when the NHAI has invited a Request for Proposal (RFP) for converting a 26-km stretch of the NH-66 bypass from Kazhakuttam to Mukkola into a four-lane road.

The NHAI’s invitation for the RFP was following the delay in handing over land for the 17.62-km stretch of the road up to Karode.

Official sources said the NHAI orders were issued on Thursday on the basis of the report given by the Competent Authority Land Acquisition (CALA).

A sum of Rs.78.60 crore would be given by the NHAI as compensation to the landowners in the Kottukal village.

Official sources said the authority would come out with an approval for the other four villages in the 17.62 km stretch once the CALA submitted the report.

The order issued by the DGM (LA & Coord), NHAI, Prag Ghosh said the compensation rates were indicated by the State on the basis of the sales statistics for similar adjoining land as on the date of publication of the statutory 3A notification on March 22, 2012, and July 13, 2013.

The rates fixed by the NHAI were Rs.8,464/sq m for dry land with PWD road access, Rs.7,618/sq m for dry land with Panchayat road access, Rs.6,671/sq m for dry land without road access, and Rs.5,925/sq m for wet land.

The local project director of the NHAI was also asked to ensure that the land was transferred into the NHAI’s possession and simultaneously mutated in the name of the government after the compensation money was deposited with the CALA.

Tharoor’s intervention

Describing it as an important day for the people, Union Minister of State for Human Resource Development Shashi Tharoor said it would bring relief to the people who were suffering for more than four decades.

With this, Mr. Tharoor said the final step for reaching the actual payments to the beneficiaries had been completed. “After receiving the payments, the land owners could go in appeal for additional compensation under various arbitration processes”, he added.

BOT project

The Public-Private Partnership Appraisal Committee of the Union government has given nod for the first 26 km of the project to be taken up on a public-private partnership mode at a cost of Rs.577.95 crore.

The entire 43.62 km stretch will cost Rs.1,170 crore.

The 43.62-km stretch from Kazhakuttam to Karode is part of the 212-km NH-66 (old NH-47) bypass project of the NHAI from Thuravur that began in 1974. It is part of the National Highway Development Project Phase III.

The 22-km first phase, from Kazhakuttom junction to Kovalam junction, was converted into a two-lane 15 years ago. Land has been acquired for a four-lane stretch and to the extent of 45 metres along the bypass on the Kazhakuttam-Chakka-Eenchakkal-Kovalam stretch.

Source- http://www.thehindu.com/

Work on Port-Maduravoyal Elevated Corridor Resumes

March 13, 2014

By C Shivakumar – CHENNAI

Photos

The much delayed Chennai Port-Maduravoyal elevated corridor project may be completed in another 30 months as the National Highway Authority of India (NHAI) resumed the work on Monday.

The work to clear way for the vehicles to ply in the area along the Cooum river has been started on Spur Tank Road, NHAI Chief General Manager (Technical), Tamil Nadu and Kerala, Chinna Reddy, told Express.

It may be recalled that following a High Court order on February 20, 2014, Reddy has stated that the work would start within three months. “But with the manpower and machinery at our disposal, the work has started with immediate effect after consultations,” Reddy said, adding, he expected to finish the project in the next 30 months.

Initially, NHAI is looking at laying the foundation along the Cooum. “One ground of land was cleared and the work began at around 11 am,” said an official at the site.

The construction of pile caps along the river stretch has been a bone of contention between the State government and the NHAI. The project hit a roadblock on March 2012 after the Water Resources Department issued a ‘stop work’ notice saying the alignment of the corridor along the banks of the Cooum had deviated from the original plan.

The biggest challenge for the NHAI is to get the slums vacated on the stretch. “There are a number of places where the slums have to be evicted by the State and the land has to be handed over to the NHAI,” said Reddy.

Other Projects

Reddy said the State government was yet to constitute land acquisition units for the 262-km Bangalore-Chennai Expressway that will run through Tamil Nadu, Andhra Pradesh and Karnataka. He said other states have already set up the units.

He also said Rs 1,000 crore road improvement project in 300 kilometres across the State would be taken up under Engineering Procurement and Construction scheme after there were no takers for Build Operate Transfer (BOT) process.

The project would be carried out in the stretch linking Madurai, Rameswaram, Karaikudi, Thanjavur and Chidambaram.

Featured Insights

- Gurugram: Hero Honda chowk to not choke anymore as Delhi-Jaipur flyover set to open soon

- Future of extensive Smart City projects uncertain

- Financiers express interest for Mumbai-Nagpur super expressway

- Indian start-ups to double by 2020: Nasscom

- SBI inks pact with IIT-Kharagpur for fintech innovation

- Supreme Court refuses to stay Allahabad HC order of making DND fly-way toll-free

- An analysis by CRISIL on the pace of road construction

- Mumbai University gives way for better connectivity at BKC

- Debit card scare: A lesson for banks and their customers

- What is a Smart City ?

The ITW Team

Sachin Bhatia Chief Editor |

Leisure

E-Z Pass Only

Improved Car Seat Belt 40% Less Accidents

NHAI's First ETC(Electronic Toll Collection) PLAZA

- ETC based on Microwave Technology(CEN 278) implemented at Delhi - Gurgaon Super Connectivity

Technology by: -Kapsch Metro JV.

News Categories

- NHAI (332)

- Highway (233)

- BOT (231)

- Projects (207)

- Default (204)

- Road (182)

- About (175)

- Infrastructure (160)

- Tolling (108)

- Investment and Finance (102)

- Expressway (98)

- Construction (90)

- Smart City (87)

- NHDP (77)

- ITS (65)

- International (55)

- Delhi (53)

- Safety (53)

- Toll Plaza (51)

- Toll Management System (50)